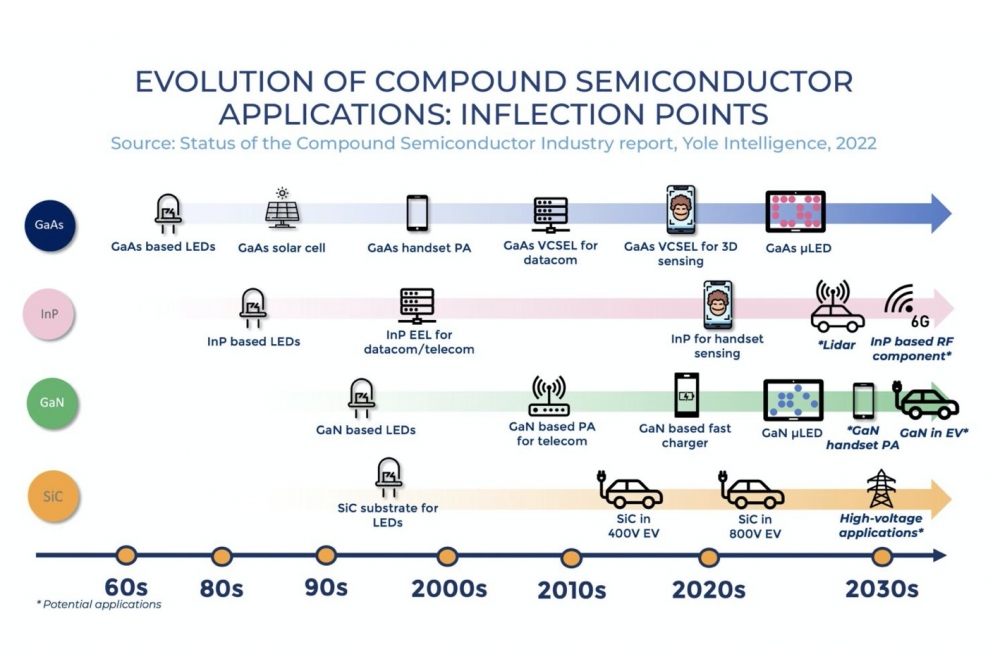

According to a new report by Yole Intelligence, the market for compound semiconductor substrate materials is projected to grow at a CAGR of 17 percent, from $945 million in 2021 to $2.3 billion in 2027. The growth is driven by increasing demand for greater power and efficiency, with SiC for power applications expected to lead the way in terms of market share among compound semiconductor substrates, growing at a CAGR of 25 percent between 2021 and 2027. In addition, the photonics InP market is expected to increase its market share and grow at a CAGR of 20 percent, while the RF GaN market is expected to maintain its market share and grow at a CAGR of 11 percent between 2021 and 2027.

The demand for SiC materials is being driven by the electrification of vehicles and high-voltage applications, leading to major players in the industry securing or expanding their substrate supply. For instance, ON Semiconductor acquired GT Advanced Technologies in 2021, Hunan Sanan Semiconductor opened a $2.5 billion Chinese SiC production line, and Wolfspeed announced a new 8 inch SiC facility in Germany to expand into the SiC device market. Infineon also partnered with automaker Stellantis to reserve manufacturing capacity and supply SiC chips in the second half of the decade to Stellantis' Tier 1 suppliers.

The RF GaN market is also expected to grow, but not in terms of market share, partly due to the impact of United States sanctions on Huawei in 2019, which affected the GaN-on-SiC supply chain. However, the market is expected to regain momentum in 2023 due to the 5G base station market in various countries.

Several companies are making moves within both the GaN and SiC markets. For example, Navitas acquired GeneSiC to launch new GaN and SiC technologies in power electronics, while Infineon Technologies signed a deal to acquire GaN Systems for $830 million, representing around 18 percent of Infineon Technologies' power electronics revenue and four times higher than the value of the entire power GaN market as of 2022.

The photonics sector is experiencing a wave of mergers and acquisitions, which is helping companies gain more market share and join competencies in key materials such as InP and GaAs. Coherent's acquisition by II-VI and Lumentum's acquisition of NeoPhotonics are examples of this trend. These acquisitions allow companies to better compete in emerging applications such as 3D sensing in smartphones and LiDAR, µLEDs, and the transition of 5G to 6G.

Apple's move towards InP-based proximity sensors in the iPhone 14 has triggered traditional GaAs players to expand their product portfolio to InP. MicroLEDs are also a significant growth vector for the GaAs photonics market, with companies such as Ams Osram constructing a MicroLED fab to supply Apple with MicroLED displays for smartwatches.

Coherent is a major supplier of SiC substrates for power and RF applications and is attempting to move from the substrate to device level. Lumentum, on the other hand, uses foundries for manufacturing before supplying devices to Apple, helping it to deal with the seasonal nature of demand in the consumer market.

Other companies are attempting to gain a foothold in additional material segments or enter the market at a different level, such as substrate, epiwafer, or process. Yole highlights 10 major CS players and their specific positions in the ecosystem. Wolfspeed's dominance in SiC and RF GaN substrates means all major device manufacturers have partnered with the company to ensure supply, and Coherent and SICC are the only other companies to offer competencies in both power SiC and RF GaN.

As CS players move to scale production on larger platforms, there is a synergy with silicon fabs that have long-established 6- and 8-inch Si processes that could be adapted for CS manufacturing. The market for CS substrates is growing as the demand for high-power devices drives manufacturing advances and sees CS players moving into different material segments.