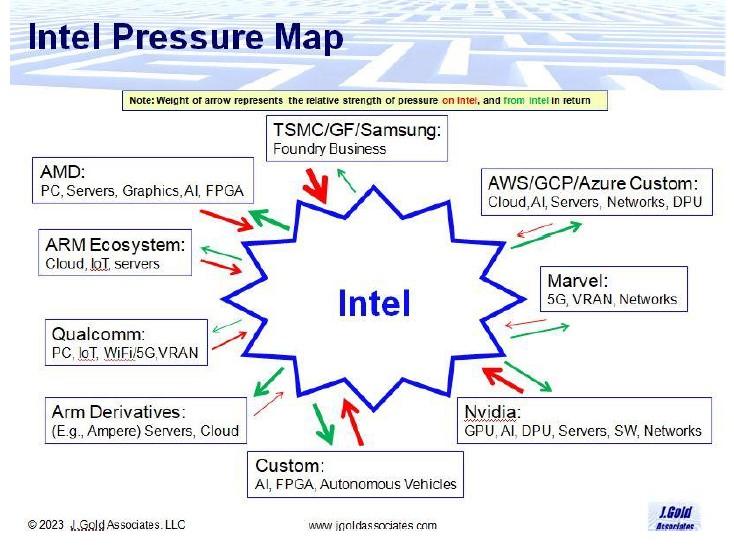

Despite being a dominant player in many markets, Intel is currently facing strong competition and numerous threats to its business. The research has revealed a "Pressure Map" outlining the areas and competitors that are posing significant challenges to Intel. However, it is worth noting that Intel is also effectively applying pressure on its competitors in several areas.

The chart shows the amount of pressure on Intel, with red representing pressure on Intel and green representing pressure from Intel. Here's an analysis of Intel's position in various market segments:

PC - AMD is increasing its market share in the competitive processor market, putting pressure on Intel's core PC business. ARM-based Windows PCs, powered by Qualcomm Snapdragon chips with 5G connectivity, are also expected to increase, although the adoption rate in enterprises is uncertain due to compatibility issues. However, there is potential for pro-sumers.

Data Center - AMD's high-performance server chips are increasing their market share and pose a threat to Intel. ARM-based CPU providers, such as Ampere, are also competing for data center and hyperscaler deployments due to their improved power/performance. However, Intel's x86 processors will likely continue to dominate due to their reliability and compatibility with existing infrastructure.

AI - Nvidia is dominating the AI market, particularly in high-end training models, but Intel has an advantage with AI accelerated CPUs for inference-based AI. Intel's Habana acquisition also provides a custom AI chip (Gaudi) that competes with Nvidia's A100 family. Low-end AI embedded accelerators in ARM-based systems may serve the lower end of the market, but Intel is expected to capture a significant share of the overall AI market.

IoT - ARM's low power approach to computing dominates in intelligent devices like security cameras and smart sensors. Intel may struggle to compete at the low end but can compete in higher-end IoT devices where compute power is critical. Intel still has potential to capture a significant share of the broad IoT market.

Edge - Intel's x86 compatibility may accelerate the deployment of enterprise software at the edge, but ARM-based servers are already powering mobile edge computing systems. Nevertheless, Intel is expected to capture a significant portion of the edge market, including deployments by hyperscalers.

Telco - Intel has benefited from being an early provider of key virtualization frameworks, such as FlexRAN, and has captured the majority of virtualized core network processing. With its new Xeon with vRAN Boost SoC, it has eliminated the need for standalone network cards. However, ARM-based suppliers, such as Qualcomm, Marvel, MediaTek, and Broadcom, remain a formidable threat in VRAN and ORAN.

Software - While Intel has produced quality software for years and made significant contributions to industry initiatives, it will have to work hard to be perceived as a competitive enterprise-level software provider. Nevertheless, this area represents a revenue growth area if Intel can be successful.

IFS - Intel has been lagging behind in process technology, but is pursuing a "catch up and surpass" strategy by opening its production facilities to outside chip companies. While it has signed high-profile companies, such as MediaTek, it remains to be seen how competitive it can be against TSMC, GlobalFoundries, Samsung, and others.

To sum up, Intel faces several challenges in maintaining or recapturing market share, but it is effectively pushing back in several key areas. While it may take a few years before all of its efforts bear fruit, we believe Intel is in a better position now than before.